Member Advantage

REPORT FROM THE PRESIDENT

First Quarter 2016

Meeting Our Mission

Our mission is to advance housing opportunity and local community development by supporting members in serving their markets. We achieve this mainly through the daily availability of our advances. But ours is a diverse membership, focused on meeting the needs of customers and communities across our District. That is why we offer a whole suite of products to help our members meet these ever-changing needs. Whether it is a First Home Clubsm grant creating new homeowners in upstate New York or Affordable Housing Program funds helping to keep senior housing in southern New Jersey, our vast product offerings help us meet our mission on a number of different fronts.

Our mission is to advance housing opportunity and local community development by supporting members in serving their markets. We achieve this mainly through the daily availability of our advances. But ours is a diverse membership, focused on meeting the needs of customers and communities across our District. That is why we offer a whole suite of products to help our members meet these ever-changing needs. Whether it is a First Home Clubsm grant creating new homeowners in upstate New York or Affordable Housing Program funds helping to keep senior housing in southern New Jersey, our vast product offerings help us meet our mission on a number of different fronts.

Last month, due to our expanded ability to issue letters of credit as collateral for deposits in the U.S. Virgin Islands, one of our members was able to provide a total of $200 million in FHLBNY stand-by letters of credit to serve as a collateral pledge for the guarantee of public funds held by it on behalf of the government of the U.S. Virgin Islands.

This represents the first Letter of Credit (L/C) of its kind that our cooperative has provided in the U.S. Virgin Islands, and is the result of an October 2015 bill which amended U.S. Virgin Islands law. The new legislation provides that a depository banking institution may use an FHLBNY L/C to secure government deposits. Previously, collateral to secure government deposits in the U.S. Virgin Islands had been limited primarily to U.S. government and agency securities, including Federal Home Loan Bank obligations. As is well documented in New York and New Jersey, an FHLBNY Municipal L/C (MULOC) is far easier to administer for both the member bank and the government. This change in the law will allow our Caribbean members to more efficiently manage their balance sheets for optimal returns by deploying less liquid mortgage loans as collateral for the issuance of the FHLBNY’s L/C to collateralize municipal deposits.

FHLBNY Announces Fourth Quarter and Full-Year 2015 Results

Our ability to expand our L/C product to the Caribbean reflects the strength of our cooperative. This strength was also on display last month when we announced our fourth quarter and full-year 2015 results.

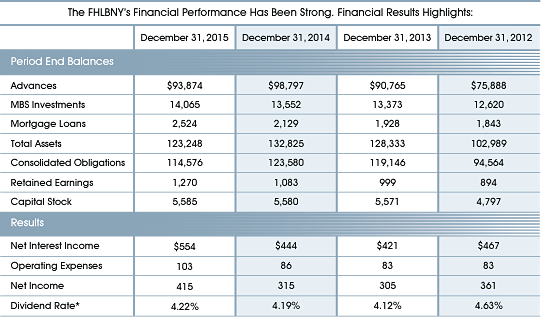

In the fourth quarter of 2015, we earned $168.4 million in net income, an increase of $91.4 million from the fourth quarter of 2014. For all of 2015, we earned $414.8 million, an increase of $99.9 million from 2014. The increase in income for both periods was due mainly to significant member prepayment activity during the fourth quarter, although our cooperative also performed very well through the first three quarters of the year. As the regulatory and competitive environment changed throughout 2015, we began to see members restructuring their balance sheets, thereby creating more prepayment activity in advances, which was reflected in the significant increase in net income during the fourth quarter.

Our strong performance in 2015 was matched by strong demand for advances, and we finished the year with $93.9 billion in advances out to our members. Our success last year will aid our community efforts this year: for 2015, we allocated $46.2 million from our earnings for the FHLBNY’s Affordable Housing Program funds that will benefit our 2016 grants.

Notes: All $ millions. *Dividends paid during calendar year.

FHLBNY Declares Fourth Quarter Dividend of 4.65

On February 18, your Board of Directors approved a dividend for the fourth quarter of 2015 of 4.65% (annualized). We continue to provide a reasonable dividend to our members, totaling more than $225 million from 2015 net income. A fair and reliable dividend is another way in which we deliver member value.

As we continue to move through 2016, our focus on enhancing this value will not waver, and all of us look forward to continuing to deliver that value to you.

Sincerely,

José R. González

President and Chief Executive Officer

FHLBNY SOLUTIONS

Considerations After the First Federal Reserve Rate Hike

One common theme heard over the years from FHLBNY members is that being highly asset sensitive and ideally poised for a rise in rates is a low risk strategy. However, we have experienced a rate environment that has left asset-sensitive members exposed to asset re-pricing, net interest margin (NIM) compression and earnings deterioration. Those members with excess unleveraged capital have forgone significant earnings during a time when NIMs were under severe pressure and regulatory and operating expenses were rising. The fact is, some members still have significant exposure to static and declining rates, and still suffer from marginal earnings and low capital growth. Are you willing to forgo earnings and suffer from marginal capital growth because you are still waiting on a substantial rise in rates?

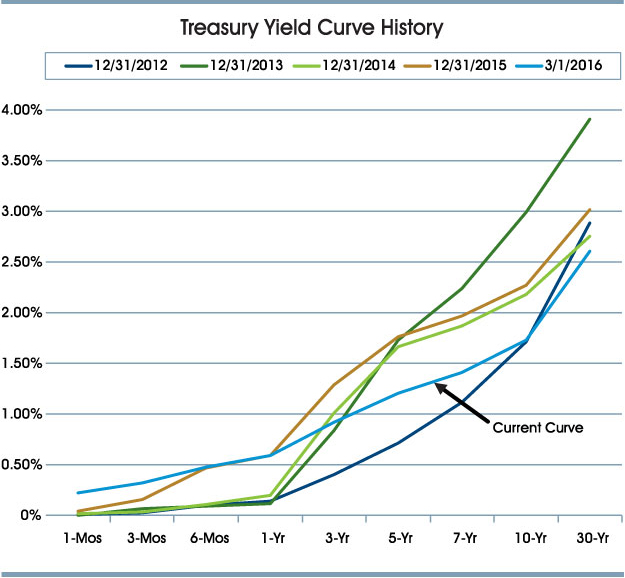

The Treasury yield curve has experienced different degrees of steepness through the past several years, but, as you can see in the following chart, today’s yield curve is at its flattest since 2012. Weak domestic growth and global economic uncertainty (marked by negative rates abroad) has caused significant pressure on the long end of the yield curve.With one Federal Reserve rate hike in December 2015 now behind us, and the Fed Funds Futures indicating there will be only one additional rate hike at year-end (68% probability), it appears that 2016 will feature more of the same — rates hovering at historic lows, a flat yield curve and continued pressure on margins and capital growth.

Data source for chart: Bloomberg 2016

Managing Your Balance Sheet For Multiple Rate Scenarios

Positioning your balance sheet for multiple interest rate scenarios is a prudent approach that mitigates over exposure to any one interest rate scenario. At this point in the interest rate cycle, it appears that most members will welcome rising rates so they can reinvest cash flows “up the curve” at higher yields. For those members that are asset sensitive, rising rates will drive up earnings. However, over the past few years, significant asset sensitivity has created exposure to a drop in rates, causing members to not realize their full earnings potential.

Consider the following solutions to position your balance sheet in this current interest rate environment.

DEPLOY EXCESS CASH

Maintaining significant excess cash reserves can be very costly. A few years ago the American Bankers Association published an article that estimated the cost for a bank to open a transaction deposit account ranged from $150 to $200, and the yearly expense to maintain these accounts was between $250 and $300. If a bank has $50 million in excess liquidity at the Fed earning 50 basis points, they would earn $250,000 annually. Let us assume the average transaction account is $5,000 and 10,000 accounts comprise the $50 million. If conservatively, the cost per account, per annum is $250 (statements, administrative costs, regulatory costs, advertising, technology, overhead, etc.), the non-interest expense associated with these funds would be $2.5 million, and would result in a “negative carry” of $2.25 million. The cost to open accounts would drive the negative carry even further (and account acquisitions were not included in this analysis).

Investing excess cash can be a first step in potentially putting your institution in a more matched position and can assist with bolstering earnings and achieving capital growth in static and declining rate scenarios.

UTILIZE CAPITAL

“With ample FHLBNY liquidity, a member does not have to live within the confines of its deposit base, but rather within their capital capabilities.”

Continuously rising operational expenses and significant pressure on NIMs have caused many members to rely on FHLBNY liquidity to help grow their balance sheets and bolster return on equity. With ample FHLBNY liquidity, a member does not have to live within the confines of its deposit base, but rather within their capital capabilities. Each member has different risk tolerance levels; however, if your institution is very asset sensitive, you may want to consider deploying your capital and investing in assets that would bring your institution’s balance sheet to a more “matched” position.

OPTIMIZE DEPOSIT PRICING

Members can test the elasticity of their deposit base with the confidence of knowing that FHLBNY funding is available to “back fill” any resulting funding shortfalls. Many members are able to achieve savings and boost margins by working their deposit base with price-tiering strategies. Additionally, the marginal cost of embarking on a deposit- raising campaign is often much higher versus borrowing from the FHLBNY. The FHLBNY has hosted several strategic financial planning workshops in the past that spotlight deposit design and pricing strategies — sessions to help members maximize net interest income. If your institution is interested, please contact your Relationship Manager.

CAPITALIZE ON LIQUIDITY

The FHLBNY has a variety of term products to assist with match funding assets that can help your institution profitably deploy capital while maintaining your desired interest-rate risk profile. The following are select FHLBNY products to consider when electing to fund long-term assets.

Fixed-Rate and Amortizing Advances

Some mortgage lenders often retain a significant portion of long-term, fixed-rate mortgage production on their balance sheet. These liability-sensitive members can elect to reduce funding mismatches and manage interest rate risk by using term Fixed-Rate Advances where they execute “laddered” strategies using a mixture of short- and long-term advances, and fund to the average life of the underlying mortgage pool. Other members choose to fund mortgages and mortgage pools with Amortizing Advances as a funding solution.

This product allows members to extinguish their advance, in whole or in part, after a pre-determined lockout period either on a one-time or quarterly basis. Members can extinguish “out of the money” advances after the lockout, or they may opt to extinguish in part should prepayments on mortgages be greater than anticipated. Callable Advances can be used to fund the “tail” of a mortgage pool should the underlying mortgages experience extension (if not, it can be extinguished). Should rates remain static, members can extinguish the Callable Advance and rebook either a new Fixed-Rate or new Callable Advance and achieve savings on the new coupon. If your balance sheet mix changes and you no longer need term funding, you may simply extinguish the advance at no cost.

Adjustable Rate Credit (ARC) Advance

This product offers an adjustable rate tied to either 1-month or 3-month LIBOR, and you can add an embedded rate cap to help limit exposure to rising rates. The ARC Advance with a cap enables members to add term floating-rate funding to the balance sheet, with the benefit of a low initial coupon rate and the protection of a cap (which allows the member to lock in a maximum rate should short-term rates increase). The embedded cap can be particularly helpful in mitigating Economic Value of Equity at Risk, as this advance becomes “in the money” when running upward regulatory shock scenarios.

Leveraging your relationship with the FHLBNY can be a critical component to thriving in this difficult operating environment. The FHLBNY is here to assist with all of your funding and hedging needs. Our products can help with mitigating risk, maximizing earnings, and positioning your balance sheet for success at different points in the interest rate cycle. All funding solutions discussed in this article should be carefully considered. If you have any questions, please contact your Relationship Manager at (212) 441-6700.

Have You Considered the Economic Impact of Your Divivdend?

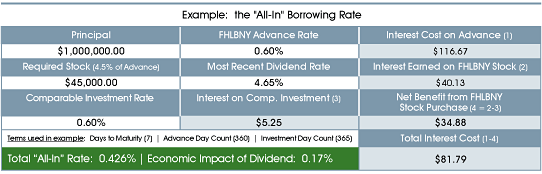

Members may wish to keep in mind the potential economic benefit of the FHLBNY’s dividend, which, depending on the advance term, can substantially lower the “all-in“ borrowing cost of an advance. The FHLBNY has an activity-based capital stock requirement equal to 4.5% of its outstanding advances. The performance of our capital stock has been historically strong, and has benefitted members by offsetting or lowering the “all-in” cost of the advance. For example, if your institution borrows a one-week advance for $1 million at 60 basis points, with a capital stock requirement of $45,000 (with a dividend yield assumption of 4.65%), the net income from the activity-based stock purchase would effectively reduce the interest expense of this trade by $40.13, or effectively lowering the “all-in” rate to 43 basis points — 17 basis points less than the coupon rate.

As illustrated in the example below, the economic impact of our activity-based capital stock can be determined by comparing an alternative investment yield to that of our dividend. Assuming you can receive an alternative short-term investment yield equivalent to the cost of the advance (60 basis points in this case), the positive spread created by the yield of our stock dividend effectively lowers the overall cost of the transaction, and quite substantially in the shorter tenors. For longer-term advances the dividend would impact the borrowing cost to a lesser degree; however, a benefit would remain and the “all-in” borrowing rate would be lower than the regular posted rate.

Please note: Although FHLBNY capital stock has been high-performing and has had a very competitive dividend rate for an extended period of time, the dividend rate is not guaranteed, and as such, it may fluctuate throughout the life of the advance. The economic impact of the stock dividend will vary based on the actual dividend rate.

HIGHLIGHTS / NEWS & UPDATES

Welcome New Members

Since our last edition, the FHLBNY has welcomed eight members into our cooperative:

ARBC Insurance Company, LLC

Cantor Real Estate Insurance Company, LLC

Nassau Educators Federal Credit Union

Palisades Federal Credit Union

Quontic Bank

Selective Insurance Company of America

Selective Insurance Company of New York

Teachers Insurance and Annuity Association of America

1LinkSK® Saving Advantage

We are striving toward full membership participation in 1LinkSK® Self Service for members by year-end. 1LinkSK Self Service continues to offer members discounted fees for transacting online.

Effective April 1, 2016, the FHLBNY is implementing a $5 increase to our Safekeeping Services fees for Purchases/Sales submitted by fax/e-mail as they require manual processing.

Updated Fees for Purchases/Sales by Fax/E-mail:

Book Entry (FED/DTC): $25 per transaction

All Physicals: $40 per transaction

Additional fee changes for trades submitted via fax/e-mail are anticipated in the third quarter of 2016, which will be communicated prior. We encourage you to utilize 1LinkSK® for all of your Safekeeping needs to save on trade fees related to manual processing by contacting our Custody and Pledging Services team at (800) 546-5101. If you have any questions about Safekeeping fees, please contact your Relationship Manager at (212) 441-6700.

FHLBNY Workshops

Could your institution benefit from a financial planning workshop?

We often design custom education programs for members to help maximize profitability.

Contact your Relationship Manager to learn more and to discuss your specific needs at (212) 441-6700.

Latest News

07/23/2025

FHLBNY Announces Second Quarter 2025 Operating Highlights

07/11/2025

$2.8 Million in Additional Funding Added to the 0% Development Advance (ZDA) Program

07/10/2025

Report from the President: Driving Communities Forward

02/22/2023

Notice of FHLB Members Selected For Community Review (Effective February 23, 2023)

07/28/2021

An Enhancement to our Callable Adjustable Rate Credit Advance (Callable ARC)