Member Advantage

REPORT FROM THE PRESIDENT

Third Quarter 2018

A Proven Partner

Last month, we reached a milestone: it has now been ten years since the conservatorships of Fannie Mae and Freddie Mac and the bankruptcy of Lehman Brothers marked both the high and low point of the financial crisis. Since that peak, our economy has made a steady recovery and is currently thriving, as are the Federal Home Loan Banks (FHLBanks). The FHLBank System has posted $1.8 billion in net income through the first six months of the year, and our “critical role” in providing liquidity to the nation’s local lenders has been recognized in positive semiannual reports from S&P and Moody’s. Most importantly, these local lenders continue to recognize the value of their membership with a FHLBank, as reflected in the strong advance demand we continue to see, with the System closing the second quarter of 2018 with $735 billion in funding flowing through communities nationwide. It is this focus on our mission – to provide funding to members in all market conditions – that kept the FHLBanks from the same fate as Fannie and Freddie during the financial crisis, and that has allowed us to serve as a proven partner to our members as we continue to work together to drive our economy forward.

Last month, we reached a milestone: it has now been ten years since the conservatorships of Fannie Mae and Freddie Mac and the bankruptcy of Lehman Brothers marked both the high and low point of the financial crisis. Since that peak, our economy has made a steady recovery and is currently thriving, as are the Federal Home Loan Banks (FHLBanks). The FHLBank System has posted $1.8 billion in net income through the first six months of the year, and our “critical role” in providing liquidity to the nation’s local lenders has been recognized in positive semiannual reports from S&P and Moody’s. Most importantly, these local lenders continue to recognize the value of their membership with a FHLBank, as reflected in the strong advance demand we continue to see, with the System closing the second quarter of 2018 with $735 billion in funding flowing through communities nationwide. It is this focus on our mission – to provide funding to members in all market conditions – that kept the FHLBanks from the same fate as Fannie and Freddie during the financial crisis, and that has allowed us to serve as a proven partner to our members as we continue to work together to drive our economy forward.

Balance Sheet Support

Advances are a key tool for members to utilize as they manage their balance sheets in our steadily improving economy. Prudent balance sheet management hinges on an institution’s full understanding of its risk profile – in static, rising and declining rate environments, as managing a balance sheet to just one rate scenario could pose significant risks and result in opportunity loss. In this quarterly newsletter, our team provides more information on how understanding the dynamics of your balance sheet is crucial to making informed and profitable risk‑return decisions, and how your FHLBNY can help.

Since emerging from the financial crisis, our members have experienced an economy marked by modest growth and very low interest rates. As a result, we have seen some of our members position their balance sheets for a rising rate environment. This is achieved by keeping their assets relatively “short,” with increased focus on consumer, commercial real estate and multi‑family mortgage lending, and a decreased desire to underwrite and retain longer‑term assets such as residential fixed‑rate mortgages or mortgage‑backed securities. Now that short‑term rates are rising, regulators are concerned about interest‑rate risk exposure in addition to liquidity and asset quality risks which may present themselves. With an improved economy, many of our members have experienced stronger loan demand. However, deposit growth has not been commensurate with asset growth, creating intense competition for deposits. Members whose business models hinge on mortgage lending can help mitigate the impacts of deposit squeeze by increasing their FHLBNY borrowing potential. This can afford members the ability to continue on a trajectory of growth, to mitigate interest rate risk and to boost on‑balance sheet liquidity.

Board Election Update

Our focus on members extends throughout our entire organization, from each business unit to management and to our Board. For more than 14 years, Anne Evans Estabrook has helped us keep that focus as an Independent Director of our cooperative. Director Estabrook first joined the Board in February of 2004, and will retire from the Board when her current term ends at the end of this year. As a champion of housing in New Jersey, she has brought her expertise on focusing on enhancing communities to our Board, most recently by serving as Chair of its Housing Committee. Director Estabrook has previously chaired the Board’s Audit Committee, and currently sits on its Corporate Governance and External Affairs Committee, Compensation & Human Resources Committee and Technology Committee. The contributions that Director Estabrook has made to our cooperative over the past 14 years have been vital to the growth of our franchise, and we are grateful for her service. We are also fortunate that Director Estabrook will continue to provide counsel to our Housing Committee and Affordable Housing Advisory Council next year in an advisory role, further strengthening our ability to meet our housing mission.

Ours is an active and involved Board, tasked with representing the needs of our members and the communities we serve, and providing management with the guidance necessary to ensure we continue to meet those needs.

On October 5, the 2018 Director Election ballots were sent to all eligible member institutions. Your responses are due by 5:00 p.m. ET on Monday, November 5.

This year, two New Jersey Member Director seats, one New York Member Director seat and two Independent Director seats are up for election. Our Board is vital to the success of our franchise, which is why it is in turn vital for our members to participate in our annual election process, and I encourage you all to do so. Whether positioning our members for long‑term success, or working alongside them to provide immediate assistance to our communities, our Board and management team constantly strive to ensure that the FHLBNY is best‑positioned to serve as a reliable partner to our members.

Sincerely,

José R. González

President and Chief Executive Officer

OUR JERSEY CITY OFFICE IS MOVING ON OCTOBER 22 TO

70 Hudson Street

Jersey City, NJ 07302

Please note the new address and stay tuned for more information.

FHLBNY SOLUTIONS

Balance Sheet Management in a Rising Rate Environment:

Will History Repeat Itself This Cycle?

After the Fed raised short‑term rates from near zero percent to now over two percent, some members are experiencing improvements to their net interest margins (NIMs) and realizing earnings and capital growth, as short‑term assets reprice “up the curve” while the cost of core deposit funding remains relatively unchanged (for now). We are just beginning to see members increase rates on their deposit accounts, focused largely on their time deposit offerings. However, we may be hitting a “tipping point” where consumers will demand higher returns on their money. Absent a steepening yield curve, NIM pressure will likely persist as the curve flattens and deposit rates rise. To optimize earnings in these challenging times, it is crucial that members fully understand their interest‑rate risk positions and utilize their asset/liability management (ALM) model as a tool to make appropriate decisions.

Are balance sheet decisions based on the assumption that rates will continue to rise, or are you making the decision to “hedge” against a static or declining rate environment? Where is your institution’s greatest degree of vulnerability, and is that exposure acceptable to you as an institution? Are you factoring lost opportunities into the equation when analyzing risk factors? The following are key areas of focus that could potentially help you thrive and reduce risk at this point of the interest‑rate cycle.

1. Keep Your Eye on Liquidity

As mentioned in the prior edition of the Member Advantage, there is a liquidity “squeeze” occurring in sectors within our district, where deposit competition is fierce amidst a period of stronger loan demand. Additional pressures are coming from new entrants such as fintech firms, which cater to consumers who prefer a more “integrated” experience where transactions can be conducted directly from smartphone devices. Furthermore, in a rising rate environment, there are concerns that liquidity outflow could occur quickly if depositors elect to seek higher‑yielding investments elsewhere, especially since smartphone devices can intensify the speed of funds transfer in this current economic cycle. Deposit outflow could adversely impact your liquidity and interest‑rate risk positions. Booking assets that could be pledged to the FHLBNY for liquidity may be a good strategy to continue your institution on a trajectory of growth. Access to FHLBNY advances could not only assist you with meeting your liquidity needs, but also with providing long‑term funding should your balance sheet require it to meet your ALM metrics. The FHLBNY would be glad to assist with conducting a review of your balance sheet to help ensure you have maximized the level of collateral pledged to the FHLBNY.

Did you know we accept 1st & 2nd lien home equity lines of credit

and expanded lendable value on Private Label CMBS?

Learn the “ins & outs” of collateral pledging with the FHLBNY.

2. Managing the Balance Sheet on a Macro Level

We find some members manage their balance sheets and make decisions on a micro level, choosing funding strategies tailored to specific assets while not properly considering macro factors that have influence. Using your ALM model as a tool in plotting a trajectory toward your income and risk targets is critical in making profitable and risk‑averse decisions. Many asset‑sensitive balance sheets can accommodate longer‑term assets without the addition of long‑term liabilities. Conversely, liability‑sensitive balance sheets may require term funding when adding certain assets to stay within risk tolerance levels. Not looking at your balance sheet on a holistic basis over the long term is “flying blind” and can be costly.

3. Understanding Risks over a Multi‑Year Horizon

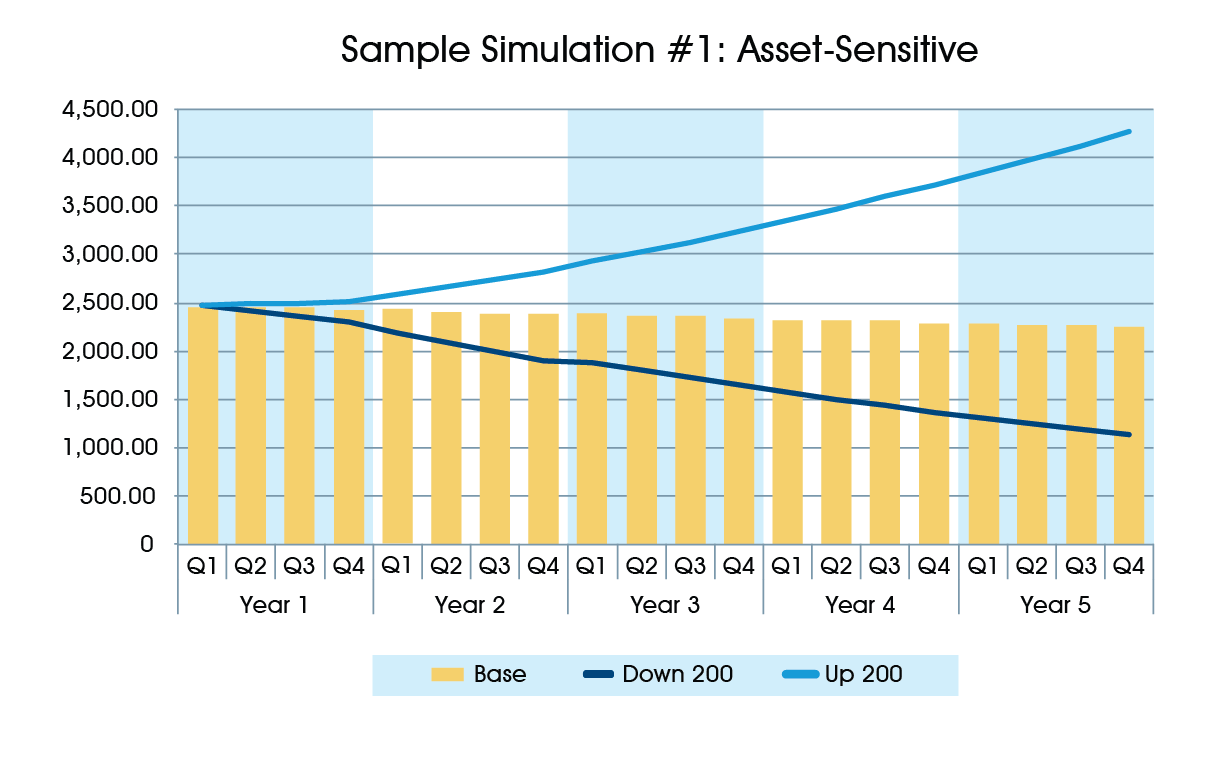

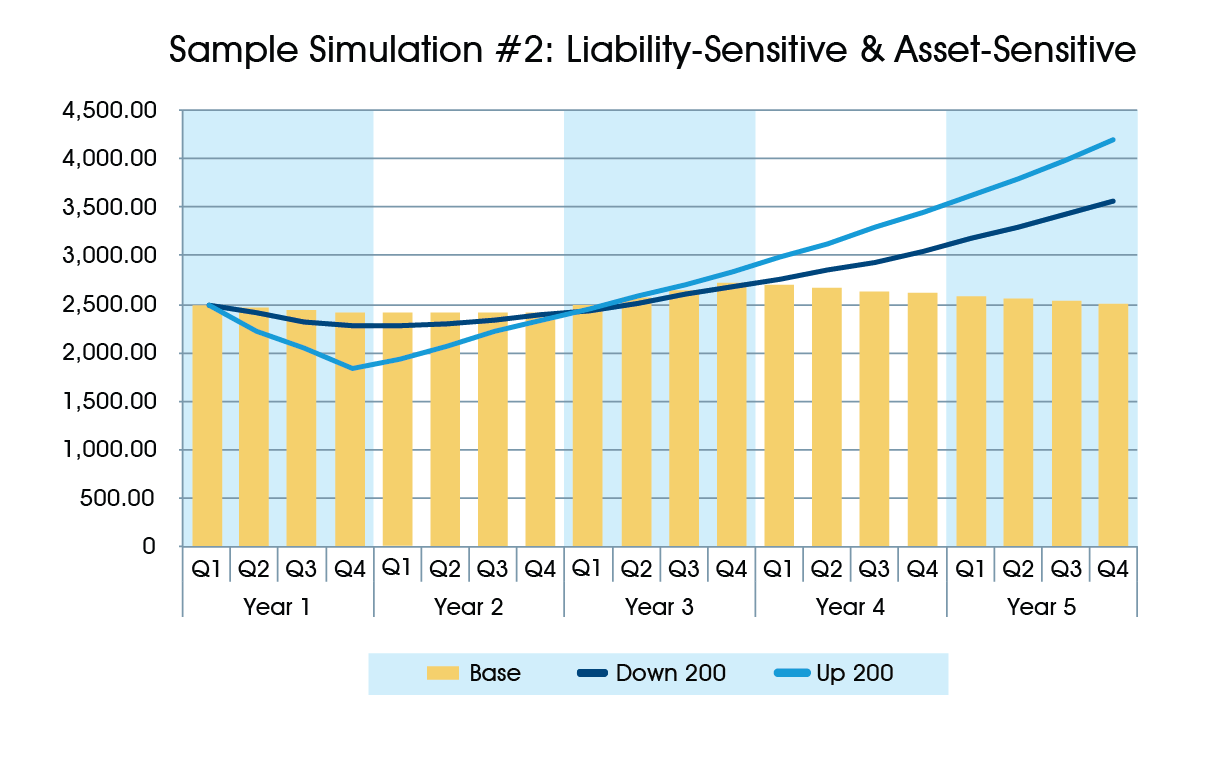

Some members tend to manage their net interest income (NII) at risk over a relatively short‑term planning horizon, such as one or two years. Two sample simulations are provided – one for an asset‑sensitive institution and another for an institution that is only liability‑sensitive in the short term.

Sample Simulation #1 illustrates an institution that appears mildly asset-sensitive, where assets reprice at a faster pace than liabilities. In this scenario, the year one story is income improves slightly as rates rise, while earnings experience modest deterioration as rates decline. However, the magnitude of risk exposure starts to be realized in year two and beyond. You can see this institution’s NII drops markedly over the next three years as rates decline, leading to an NII that is roughly half of the base case by year five. The balance sheet behind this illustration could potentially support longer‑term assets that could be funded with short‑term advances. Such action could potentially lead to a more “matched” position; the interest rate risk profile would improve since you’d be guarded against a declining rate environment, experiencing improved earnings in a flat rate environment and modestly rising rate scenario. Also, assuming you have underutilized long‑term “core deposits,” spread on the additional long‑term assets could be preserved because the betas on these deposits are generally very low in a rising rate environment.

Sample Simulation #2 illustrates an institution that is considered to be liability‑sensitive in the short term, susceptible to rising rates as liabilities reprice at a pace faster than assets. However, in this illustration, the institution is liability‑sensitive beginning in year one into year two. It starts to reap benefits from rising rates in year three and beyond, where the balance sheet becomes asset‑sensitive and NII begins to surpass the base case scenario. If this institution solely focused on the short‑term, they would potentially make uninformed decisions using incomplete data, leading them to believe they could reduce risk by reducing long‑term assets or adding long‑term liabilities.

This sample balance sheet may call for adding longer‑term assets, such as funding with term FHLBNY advances out to the two‑year point, hedging the period of time that is susceptible to NII deterioration. Longer‑term assets could potentially protect this balance sheet from declining rates and improve earnings in a static and even rising‑rate environment. Being properly informed could potentially help you achieve greater NII, mitigate risk and put your institution on the path to improved earnings and capital growth in most scenarios.

4. Proper Utilization of Core Funding

Breaking down the composition and attributes of your deposit base and understanding how “core” and “non‑core” deposits fund your asset categories is an important exercise when conducting planning. Core funding, which is generally not rate sensitive with a long‑term average life, is often underutilized. We have seen members use these long‑term deposits to fund short‑term assets at disproportionate levels. For example, a member may be funding their balance sheet entirely with core funding, yet focus on short‑term lending such as auto, consumer and floating rate home equity lending. This strategy may work well in a rising rate environment as spreads widen; however, in static and declining rate environments, members may be left vulnerable to NII deterioration and lose earnings opportunities. With an underutilized base of core funding, diversifying the balance sheet could potentially add more long‑term assets, boosting income in static, declining and even upward rate scenarios. Even in a rapidly rising rate environment, spread associated with long‑term assets could persist due to low betas traditionally associated with core deposits. And in an environment of intense competition for loans, short‑term assets may not reprice upward as quickly as anticipated because lenders may have to settle for lower spreads to “win” deals. To plan for multiple scenarios, consider working toward becoming better “matched” from an ALM perspective by utilizing core funding to book longer‑term assets. This could potentially lead to greater earnings, capital growth and a reduced risk profile.

5. Being Mindful of Potential Pressure on Asset Quality

Short‑term loan portfolios produce constant cash flows that can get re‑invested up the curve in a rising‑rate environment. This can enhance profitably as rates rise. However, exposure to asset quality risks may escalate as consumers’ average monthly payments rise on short‑term loan products. The desire for short‑term assets by financial institutions has been substantial during the “post‑financial crisis” years, as the industry was waiting for the arrival of a rising‑rate environment. Consider diversifying your balance sheet in longer‑term mortgage products that have a reduced credit risk profile. These products can be pledged to the FHLBNY to maintain liquidity, can serve to anchor your balance sheet, and can optimize earnings in a static, declining and potentially rising rate environment.

NEWS / HIGHLIGHTS

Welcome New Members

Since our last edition, three members joined the FHLBNY cooperative:

Corporation for Supportive Housing

Horizon Healthcare of New Jersey, Inc.

St. Pius X Church Federal Credit Union

CONNECT WITH US

We stand ready to serve you at all points of the interest rate cycle.

Member Services Desk: (212) 441-6600 | Relationship Managers: (212) 441-6700

Have suggestions for a future topic? E-mail your thoughts to [email protected]

Latest News

07/23/2025

FHLBNY Announces Second Quarter 2025 Operating Highlights

07/11/2025

$2.8 Million in Additional Funding Added to the 0% Development Advance (ZDA) Program

07/10/2025

Report from the President: Driving Communities Forward

02/22/2023

Notice of FHLB Members Selected For Community Review (Effective February 23, 2023)

07/28/2021

An Enhancement to our Callable Adjustable Rate Credit Advance (Callable ARC)